How Tissot’s India Infrastructure Turned A Promising Market Into A Structural Growth Engine?

Part-II of a Four-Part Research Series

Tissot’s India numbers suggest that in this market, building infrastructure before demand is not a gamble, it is a strategy that is already paying out in hard revenue.

Building the rails before the traffic.

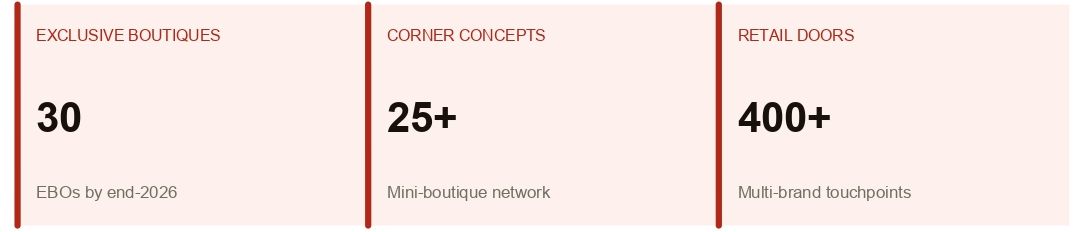

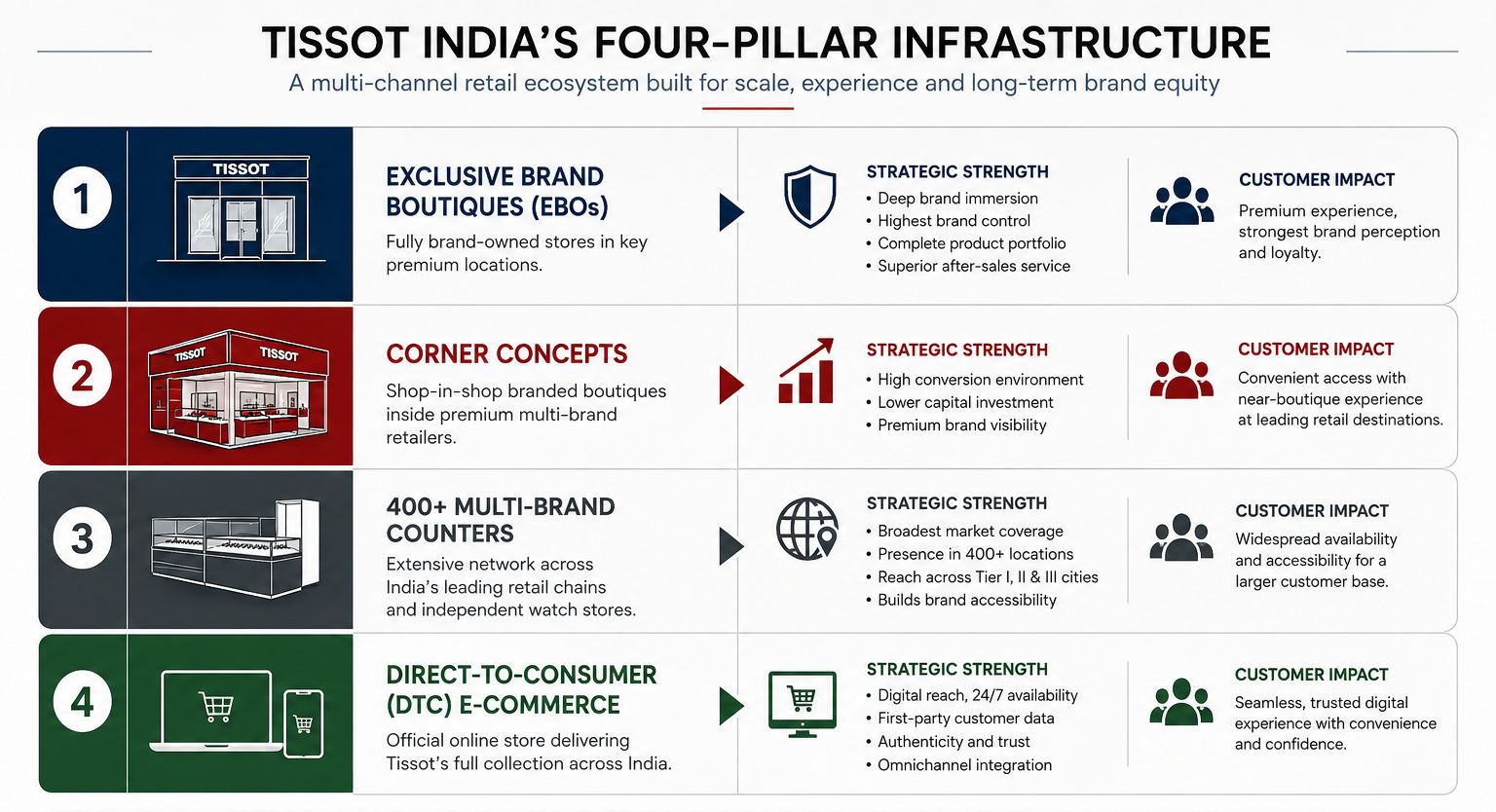

The data reads almost like a playbook in “infrastructure as moat.” By end 2026, the brand is expected to operate 30 Exclusive Brand Outlets (EBOs), more than 25 Corner Concept mini boutiques, and over 400 multi brand retail doors across India - collectively the deepest Swiss watch retail network in its price band.

This is not just marketing flourish, it is the foundation of a distribution system designed to be in place before the market fully matures. Tissot’s consumer turnover is estimated at roughly Rs.700 crore in FY2025, with the same estimated to reach about Rs.1,000 crore in FY2026, and this impressive jump is a direct consequence of DTC going live, the EBO and Corner Concept rollout, and the onset of EFTA duty reductions.

Tissot has a mission of offering millions the joy of wearing a Swiss watch, crafted with quality and beauty that honor its legacy, and embodying Swiss values of precision, innovation and tradition. This matters because it explains why the company invests in physical and digital presence at a scale usually associated with mass brands: the goal is not exclusivity through scarcity, but Swiss precision at scale, delivered through infrastructure that can reach aspirational buyers across cities and channels.

Tissot India - Infrastructure Snapshot (By End 2026)

Channel type | Count / Status | Strategic role |

Exclusive Brand Outlets (EBOs) | 30 stores | Full brand experience, control over merchandising |

Corner Concept mini‑boutiques | 25+ inside multi‑brand stores | High‑conversion “brand islands” in shared spaces |

Multi‑brand doors (authorized) | 400+ counters | Breadth of presence in metros and Tier‑2 cities |

DTC e‑commerce platform | Launched April 2026 | Direct data, margin, and authenticity control |

EFTA duty‑reduction phase | Starts 2026 | Lower landed cost of Swiss watches over time |

The Corner Concept As Conversion Engine

One of the most defining entities about the Tissot’s India performance is not about turnover, it is about what happens on the shop floor. Across premium multi brand stores - Ethos, Helios, and authorized counters in metros and Tier 2 markets - retail intelligence consistently places Tissot as the highest converting Swiss brand in the Rs.25,000 - Rs.1,00,000 segment, with walk in customers often arriving “brand decided,” particularly for PRX and Seastar. A brand report states that Corner Concept mini boutiques inside multi brand environments deliver substantially higher conversion rates than standard counters, effectively turning generic watch traffic into first time Swiss buyers at a higher clip.

This matters for infrastructure strategy because it shows that Tissot is not just adding points of sale, it is engineering different types of retail real estate to play different roles in the funnel.

- EBOs act as fully controlled brand environments in prime locations.

- Corner Concepts function as embedded boutiques inside larger watch ecosystems, positioned in cities like Pune, Ahmedabad, Jaipur, Raipur, Kochi and Chandigarh - markets where a full standalone store is the “natural next step.”

- Standard counters extend reach but do less of the heavy lifting on conversion and storytelling.

For a market still warming up, this is an unusual level of nuance. Many brands treat India as a handful of flagship stores and wholesale relationships. Tissot’s approach resembles multi format retail strategy from mature markets, transposed into an emerging context.

DTC As The Fourth Pillar

Infrastructure in India is no longer just bricks and mortar. In April 2026, Tissot became the first Swatch Group brand to launch a brand owned, direct to consumer e-commerce platform in India, shipping from an India based warehouse and accepting UPI and card payments.

The brand estimates e-commerce - including DTC and authorized online channels, at about 10% of total India consumer turnover in FY2026, or roughly Rs.100 crore, and explicitly links this new digital layer to improved margins, direct customer data, and full control over the brand journey from discovery to purchase.

This dovetails with key Indian luxury watch market takeaways in a couple of ways.

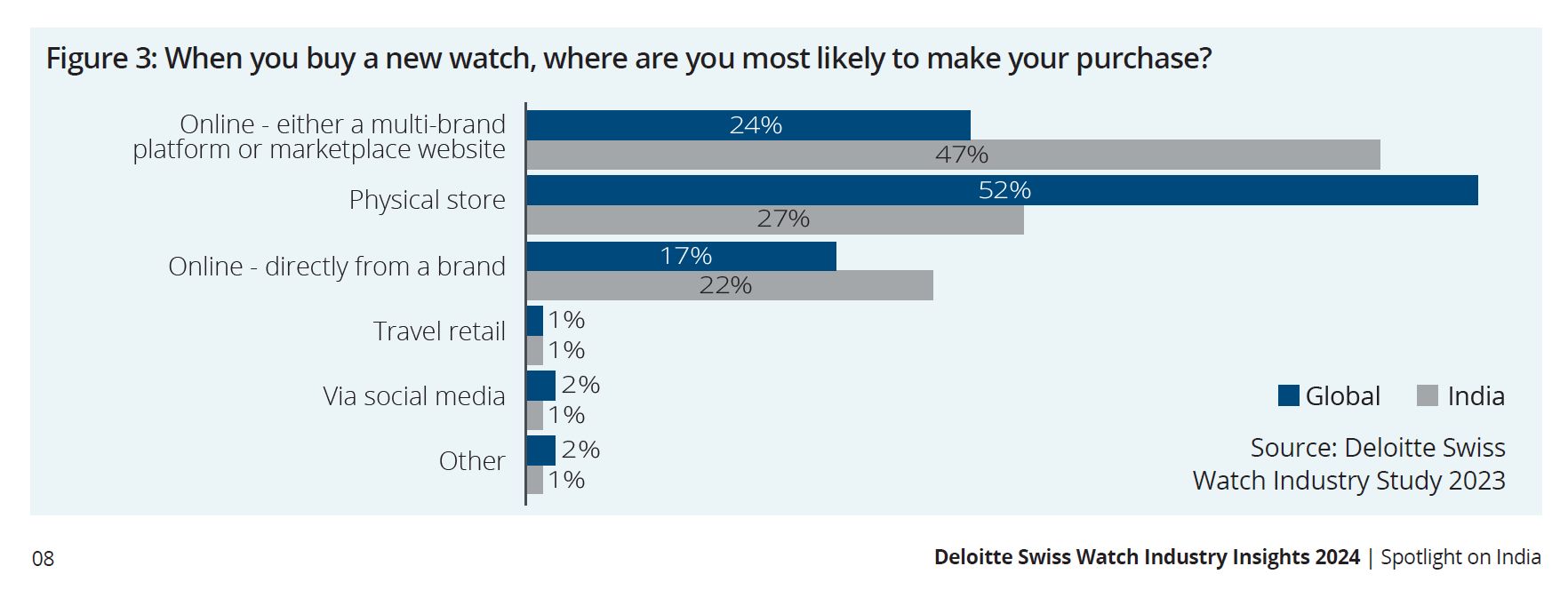

First, Deloitte’s “Swiss Watch Industry Insights 2024: Spotlight on India” notes that Indian consumers increasingly research watches online before buying, and that younger buyers are particularly comfortable blending digital discovery with offline as well as online purchase.

Second, India’s overall watch market, valued at about USD 3.2 billion in 2024 and projected to reach roughly USD 5.13 billion by 2033 with a CAGR of 5.28%, is seeing a structural shift toward organized and omnichannel retail, with branded and luxury watches capturing a growing share of value even as mass segments remain volume driven.

By putting its own DTC platform into that ecosystem early, and making it part of the same infrastructure stack as EBOs and Corner Concepts, Tissot is doing more than selling online. It is creating a fourth pillar in a distribution moat that extends from high street boutique to smartphone screen.

Tissot India’s Four Pillar Infrastructure

Here’s a structural chart laying out Tissot India’s four-pillar retail infrastructure, with each pillar's role and reach at a glance. These pillars form overlapping coverage across India’s emerging premium watch consumer base.

A Market That’s Expanding Underneath The Infrastructure

Infrastructure is only an advantage if the market beneath it is expanding. Here, the macro data is unusually supportive.

Deloitte’s India spotlight identifies several demand side drivers:

- Watch and luxury markets growing in India, supported by GDP growth, urbanization, and rising discretionary incomes.

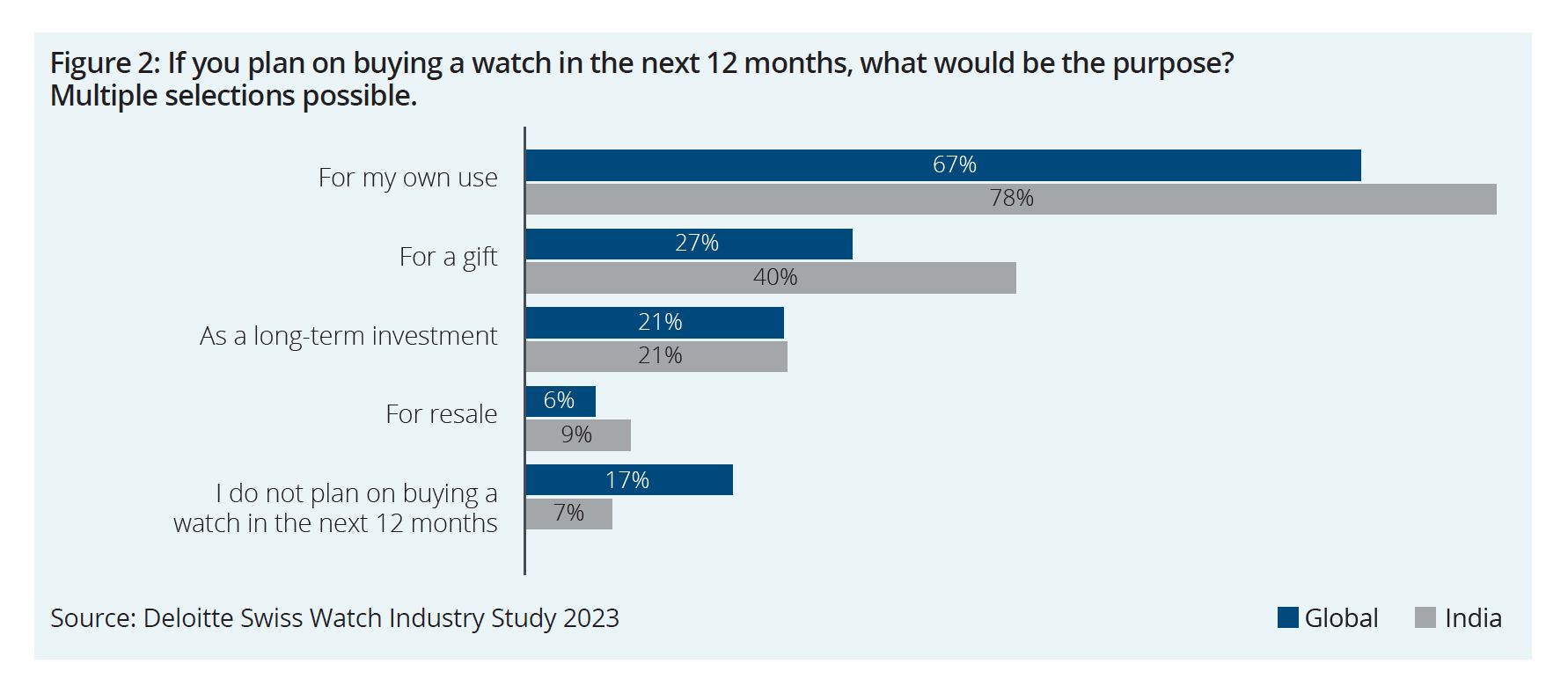

- Consumers “aspire to luxury,” with a significant share indicating they plan to buy watches primarily for their own use, but also as gifts and long-term possessions, not just devices.

- Global brands entering the stage, and Indian consumers increasingly aware of - and receptive to - Swiss names.

Tissot’s infrastructure strategy is targeted squarely via a network that is built to serve the buyer who wants the joy of wearing a Swiss watch, with precision, innovation and tradition baked in, rather than the buyer seeking another notification platform.

Regulatory Tailwinds And Supply Chain Readiness

On the supply side, timing also matters. From 2026 onwards, the EFTA trade agreement begins to reduce duties on Swiss watch imports into India, widening the addressable market by making Swiss watches marginally more affordable or more profitable, depending on pricing decisions.

This sits on top of Swatch Group’s global infrastructure: USD 6.9 billion in global consumer turnover in FY2025, world class movement manufacture, and centralized quality assurance and logistics.

Tissot’s four-pillar retail infrastructure means that the foundation is already laid to carry increased Swiss watch inflows and convert them efficiently into retail turnover. That readiness turns policy tailwinds into practical advantage.

A Different Idea Of Luxury, Delivered Through Infrastructure

Underlying all of this is Tissot’s own view of what it is trying to do.

Rather than defining itself through rarity and high price, the brand describes its mission as bringing Swiss watches - crafted with quality and beauty that honor its legacy - to millions, and embodying precision, innovation and tradition in every creation.

In India, that philosophy is expressed through infrastructure: the decision to put Swiss precision within reach of a much larger audience by investing in the places and platforms where those audiences actually shop.

In a global industry where many luxury strategies still revolve around scarcity, Tissot’s India story is a reminder that there is another way to build a valuable brand:

- Make the product technically credible and symbolically strong,

- then build a distribution moat so deep that when the market finally catches up, you are already everywhere it needs you to be.

For India’s watch market that is perhaps the most important takeaway from Tissot’s growth: the rails are already here, even while the traffic is only just gathering pace.

For Part-I of this four part research series, click here.